Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

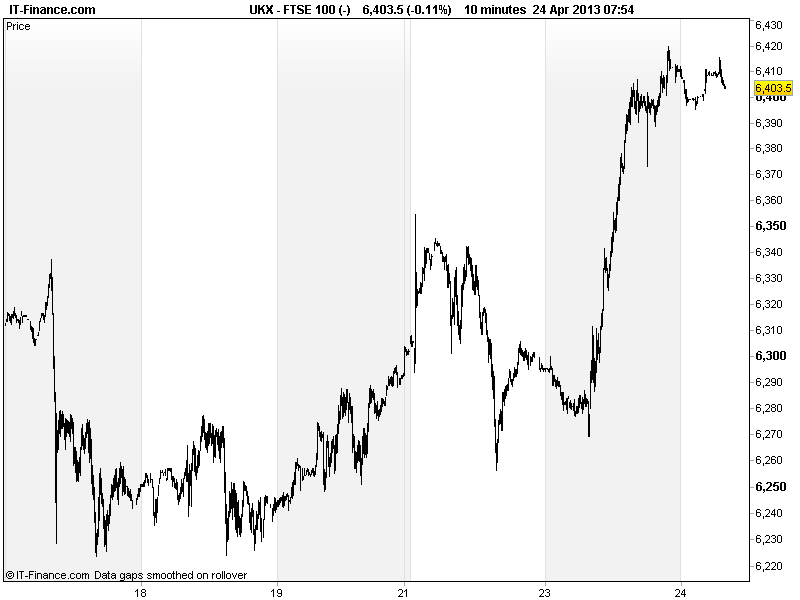

UK 100 called to open +15pts, maintaining the key 6400 level helped by outperformance by equities in Asia, with Australia assisted by weaker than expected after lower inflation reduced the chance of a rate hike (AUD/USD slipped marginally). Neighbour New Zealand held rates and gave a more upbeat economic outlook.

After hopes an ECB rate cuts yesterday following poor PMI data from Europe, US and China, loose monetary policy still very much a driving force of optimism, helping keep risk appetite buoyed. Japan still doing well helped by aggressive BoJ policy aimed at economic rebound rather than competitive devaluation, while China recovering some recent losses.

Overnight sentiment also boosted by Apple Q2 results, with beats for revenues and profits, and an increase in share buyback and dividend, but the outlook disappointed, with Q3 guidance below expectations and suggesting no major product launch.

S&P’s threat that Australia could lose AAA rating within 5 years (as national debt climbs) had little effect, suggesting such a time-frame is well beyond that of the average current investor. Europe still benefiting from solid peripheral debt auctions on lower yields while in Italy, after President re-instated, expected to appoint new PM and hopes political deadlock resolved.

Markets wobbled last night though after the official Twitter account of Associated Press was hacked and a fake tweet posted suggesting an explosion at the White house which saw the Dow Jones plunge 140pts briefly before recovering fully. Social Media’s influence within finance likely to come under more scrutiny.

In focus today will be the German IFO Surveys (seen edging down), especially after yesterday’s PMI data for the nation disappointed and boosted hopes that the ECB could cut rates (denting the EUR/USD, helping equities) to boost the region, as austerity bites hard.

US Durable Goods Orders seen falling back after last month’s strong growth, although excluding transport the measure is seen rebounding. Lots more Q1 Results flowing through form the US with names such as Whirlpool, Motorola Solutions, Sprint Nextel, Ford & Boeing all updating the markets on.

UK 100 regained key 6400 level however slowed up as resistance encountered at mid-month. Nonetheless, bulls pleased by recent falling highs trend being broken yesterday. Potential for bigger 6215-6400 sideways channel to emerge, but appetite still strong and so equal possibility of rally back towards highs of 6500.

Gold rebounded from yesterday’s lows of $1405, maintaining recovery from recent extreme sell-off to 2yr lows of $1321 and likely helping form support at $1400. Resistance likely around $1500 and $1550 round numbers.

In Oil, Brent Crude still trading sideways within $99-101 range, not benefiting as much as equities from renewal of risk appetite. US Light Crude doing the same, trading around $88 with resistance at $89 but support much lower at $86.

In FX, GBP/USD back down below 1.53 but with 1.52 still potentially supportive. Expectations of GDP releases from the two nations later in the week, outlook for QE and demand for the greenback as a safehaven could dictate direction. EUR/USD back around $1.30 on expectations of ECB rate cut following poor regional macro data.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan Corporate Service Price Index Better

- Aussie DEWR Internet Skilled Vacancies Rebound

- Aussie Consumer Price Index Worse

- Switz UBS Consumption Indicator Decline

- Switz Credit Suisse Q1 Results Worse

- Germany Daimler Q1 Results Worse

- UK Barclays Q1 Results Worse

- See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- BAE Systems, suppliers warn of fallout from Bradley shutdown

- Lloyds UK branches sale to Co-op collapses –sources

- Shanks exits from UK landfill

- Sports Direct Q4 sales up 14.3 pct

- Blinkx upgrades year outlook

- Pace sees first-half revenue ahead of last year

- Takeover panel extends CPP offer deadline

- Barclays Q1 profit hit by restructuring charge

- Kier says on course to meet FY expectations

- Kier makes recommended offer for May Gurney

- Virgin Media Q1 free cash flow up 54 percent

- Computacenter reports flat first-quarter revenue

- Reed Elsevier’s first quarter revenue growth in line with 2012

- Gem Diamonds says quarter grades reduced in line with view

- Statoil drills dry well in North Sea

- DS Smith expects full-year operating profit in line with expectations

- Range Resources to merge with International Petroleum

- Fenner first half profit falls, co expects return to growth next year