Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires

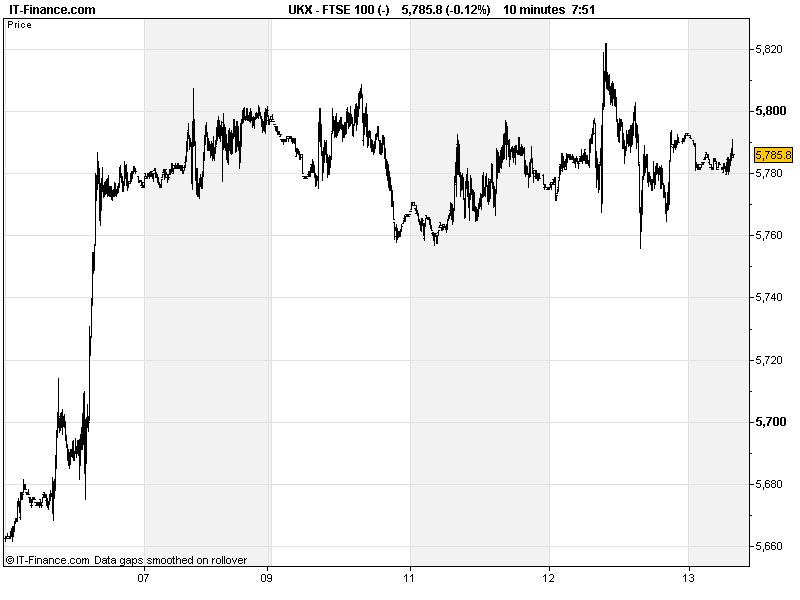

UK 100 called to open +10pts, after US and European markets finished slightly higher, following relief at Germany’s constitutional approval (albeit with conditions attached – still holding purse strings!) of the new European bailout fund, European Stability Mechanism (ESM) and fiscal pact, potentially taking the troubled region a step closer to a more solid backstop and European Central Bank (ECB) intervention to appease borrowing costs where necessary. Some M&A talk also provided a boost to sentiment (BAE Systems and EADS).

Expectations still running high that the US Federal Reserve (Fed) will announce further Quantitative easing (QE)/stimulus measures to boost the US economy. It’s not a done deal, although you might think so given the weakness of the US Dollar (USD) and price of gold.

There is still a flow of US macro data which could counter the need (nothing great, but not disastrous either), however, the growing dovishness of comments from the Federal Open market Committee (FOMC) and their increasingly ‘ready to act’ stance has seen markets pretty much price in a move. If anything, real reaction would likely now come from Fed inactivity (another delay?).

Then again, both the Fed and ECB have proved recently that words can mean more than action with both having done nothing for a few months and yet markets happy with intentions, expectations, and backstops. This could well continue.

Overnight in Asia, equities mixed suggesting caution ahead of this evening’s big event, but overall expectations that US and China will take additional measures to boost economic growth, although official Chinese news agency has stated that massive stimulus could be ‘detrimental’ to sustainable economic growth, suggesting help may not be as forthcoming, while other reports point to measures being announced to stabilize foreign trade. Nice and clear, as usual.

Apple’s launch of the iPhone 5 saw mixed reaction in the tech world with many disappointed at yet another incremental product update. Back in Europe, Dutch elections show pro-Europeans remaining at the helm, providing a boost to the region which views the nation as an in indicator of Europeans voter’s attitudes to proposed further integration (more federation).

Earlier speculation (conflicting) that Spanish PM Rajoy may be considering asking for Eurozone help in order to get the ECB to intervene in bond markets have been followed up by Bloomberg reports that France could be pressing Spain to snub German concerns and go ahead and ask, in order to contain the crisis.

Note that the Bank of England’s (BoE) quarterly bulletin points to inflation remaining volatile (although not necessarily higher) and the likelihood is that the Monetary Policy Committee (MPC) leaves policy looser for longer.

In Commodities, Gold found support at $1,725 after its fall from $1,745 and trading flat in anticipation of this evening’s effects on the US Dollar (USD). Its cousin Silver shows similar moves, although with more volatile moves. Oil (US Light Crude and Brent) off their highs but at upper end of week’s range. Note that Fed stimulus would likely weaken the dollar to makes commodities cheaper to help with economic growth, however oil is not exactly ‘cheap’ at the moment – near recent highs, which would surely hike inflation again to the detriment of consumers. Double-edged sword this stimulus.

In FX, USD still weak vs GBP, with GBP/USD above 1.61 on stimulus expectations. Could May highs of 1.63 count for anything in terms of resistance? EUR/USD pair now above 1.29 on combination of stimulus expectations, European Central Bank commitment and German approval of ESM, as well as continued speculation that Spain makes official request for help. But resistance a long way off (1.35) given the regions recent woes.

In today’s macro line-up, data likely to be overshadowed by the Fed rate, QE decision and economic projections after the European close. Nonetheless, data-points to watch include US Producer Price inflation and Unemployment, and debt sales by Italy (medium term) and Ireland (short-term). European leaders Monti (Italy) and Merkel (Germany) are scheduled to speak. Note also that we have the publication of the ECB’s monthly report which will add to the current central bank focus.

Should you require any other help on what’s moving the markets, speak to you friendly trader.

Overnight/Weekend Macro Data: (Source: Reuters/DJ Newswires)

- Aussie CPI Expectations In-line

- See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Dunelm FY profit up 15 pct

- Kier says final dividend at 44.5 pence per share

- Imagination Tech on track for 1 bln shipments by 2016

- Anite says four-month trading ‘encouraging’

- Premier Farnell Q2 profit slips by 20 percent

- Next says August, Sept sales disappointing