Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

UK 100 called to open -15pts, with Asian bourses mixed overnight despite Wall Street pushing to new record highs (note: fueled by defensives) and concerns on Cyprus receding, but with worrying sabre-rattling continuing on the Korean peninsula.

Japan’s Nikkei outperformed on expectations that tomorrow’s BoJ policy meeting could provide aggressive monetary easing (boosting asset purchases). In Australia, equities weak despite an improved trade balance.

Key macro data overnight comprised updates from China where we saw improvements to a 6-month high for the official Non-Manufacturing PMI and 2-month highs for the HSBC Services PMIs suggesting robust March growth despite new property curbs, potentially putting at ease those concerned growth in the world’s #2 economy was at risk.

In the UK, BRC Shop Price Inflation accelerated in March with the impact of weak GBP beginning to impact import prices something which may continue to flow through next month maintaining pressure on the already squeezed consumer.

In the commodities space, weakness in Gold (sub-$1575) stemmed from talk of QE tapering during a face-off between non-voting Fed members Evans & Lacker with the former envisaging strong US growth not stalling in H2 and the latter upbeat on current macro data and favours a reduction in QE this year depending on data.

In focus today will be the UK PMI Construction reading which is expected to improve, but remain sub-growth. Eurozone Consumer Inflation is expected to have softened in March reducing any calls for any ECB rate cut.

This afternoon, ADP Employment seen remaining around 200K and likely generating much discussion ahead of Friday’s Non-Farm Payrolls. Continuing the Non-Manufacturing data run, US ISM is seen ticking back a bit but staying very much in growth territory.

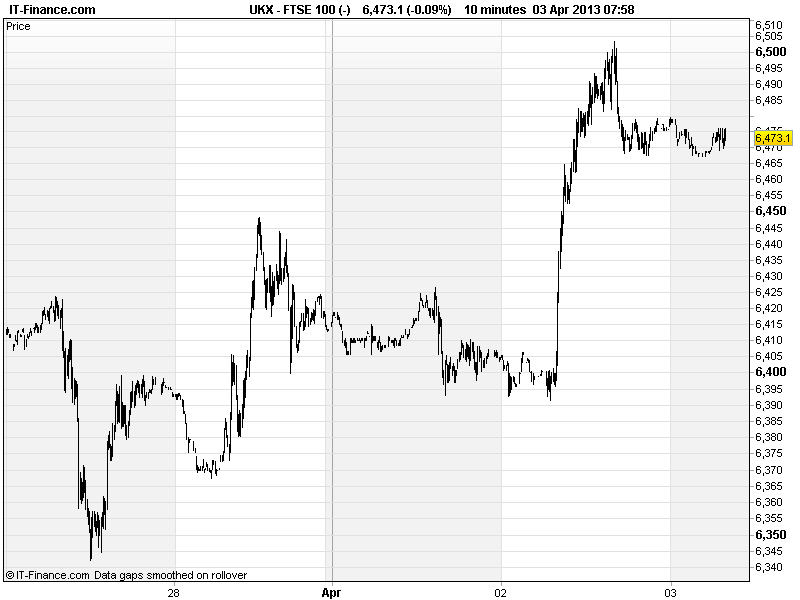

UK 100 has rallied back to 6500 level and broke above 2-week Cyprus influenced highs of 6480. Back around this level overnight and key will be whether the breached highs (1-week 6460, 2-week 6480) can act as support and help with a renewed push back towards March and 2013 highs of 6550. Having sat between 6340-6480 for a fortnight, any market worries could easily put the index back in this range again.

Gold weak on prospect of QE tapering from Fed member comments and stronger USD. Watch Feb lows of $1555 for support, but possibility that rally $1575-1615 was bearish flag after declines form $1680 and downside possibility to $1500, helped by combination of safe-haven seeking and stronger USD.

In Oils, US light Crude remains near end-March highs of $97 with potential support at $96 and resistance $97.5. Its cousin Brent Crude off its highs but retains uptrend from 24 March with support around $111. Both remain upbeat amid environment of mixed macro data.

In FX, GBP/USD fallen below 9-day support at 1.51 as USD benefits from demand for the greenback. Note mid-March support around 1.5075 and resistance at 7-day highs of 1.525. As for EUR/USD, it is still hanging around 1.28 following Cyprus resolution. Still in 2-month downtrend with 1.30 handle and 200-day moving average now major horizon hurdles.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- UK BRC Shop Price Inflation Accelerated

- Aussie New Home Sales Deteriorated

- Aussie Trade Balance Worse, but improved

- China Non-Manufacturing PMI Improved

- China HSBC Services PMI Improved

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Babcock bid pipeline increases to 15.5 bln stg

- Interserve forms jv to invest in Edinburgh’s Haymarket

- Thorntons sees FY profit ahead of expectations

- GW Pharma gets new US patent allowance for delivery of Sativex

- Great Portland acquires 148 Old Street

- Keller wins £35M contract in Russia, largest to date

- UK energy regulator fines SSE for mis-selling

- Rio Tinto hires Deutsche Bank for Australian coal asset sales –report

- Prudential buys rental homes from Berkeley Group for £105 mln