Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

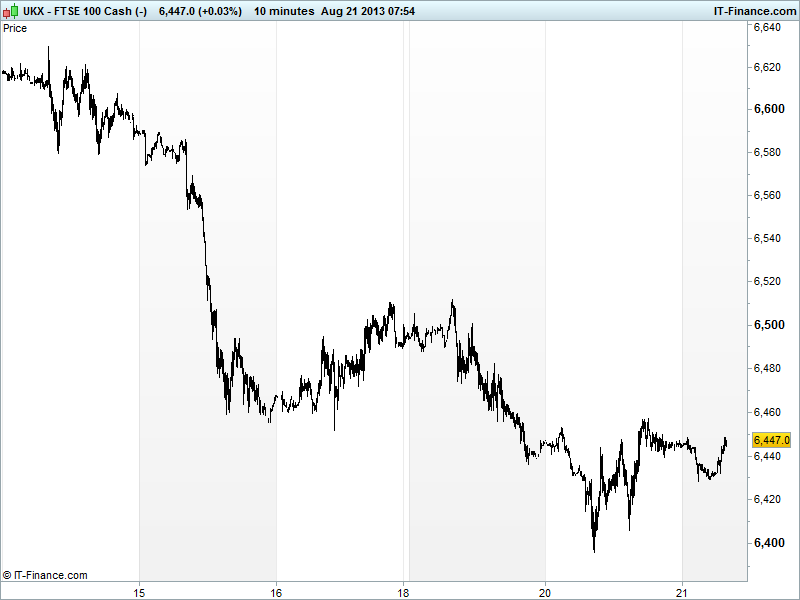

UK 100 called to open +10pts at 6445, with 6400 having held up yesterday and breakdown level of 6460 tested as taper tantrum sell-off ahead of release of Fed minutes this evening eased and US markets closed largely positive, putting Asia (ex-Hong Kong) in the green, after solid results from retailers such as Best Buy and ratings agency Moody’s upgrading outlook for US states to Stable.

Asia mixed on news that severity of latest Fukushima nuclear plant leak (radioactive water) raised from 1 to 3 (serious incident) and Hong Kong in the red with Chinese equities lower, although off worst levels as Fed tapering now perceived as priced in and Bloomberg report that economists expect 7.5% 2013 GDP growth as achievable as economy stabilises. China and Japan in discussions to prevent another escalation of the tensions surrounding disputed islands.

BoJ governor Kuroda reiterated policy will be adjusted if economy and inflation don’t improve as expected, notably if downside risks from proposed sales tax hike or deterioration in global economic stability, which goes some way to offset the prospect of lost stimulus from the US tapering and the beginning of the end of global loose policy which is spooking markets and assets worldwide.

In focus today, as if anything could garner more attention than Fed minutes, where more clues well be sought on taper timing, we caution against expecting too much given that these are from July and much water has since passed under the macro data bridge. Latest consensus is 65% expecting a September tapering to $75bn from current $85bn.

Otherwise, for data-watchers we have UK Public Finances where are seen improving yet further, which could continue to benefit GBP vs. peers such as USD and EUR after the recent breakouts. UK CBI Trends are also seen better than last month as confidence in UK recovery grows.

US Existing Home Sales are seen resuming growth after a down June, as consumer confidence grew, although caution to the fore after recent taper-fuelled spike in US treasury yields likely now impacting financing costs and weighing on August/September prints. Results season continues with big names Hewlett Packard, Target, Staples and Loewe’s updating later.

UK 100 off its worst levels of 6400 (200-day MA and historical trendline held) and back above the trendline of falling lows which it broke below as the taper tantrum accelerated yesterday. Overnight the 6460 level we broke down from o Monday has been tested as buyers return, considering the sell-off overdone and with the possibility of now dated Fed minutes providing no additional worries, merely confirming current market expectations. A break above 6460 could see upside to late last week and Monday’s highs of 6510, possibly even 6560. Without another breakout though, pressure remains.

In FX, GBP/USD still gaining ground at 1.567 after recent breakout at 1.555. Next hurdle a cent away at June highs 1.575, while 61.8% Fibonacci retrace of fall since beginning of year could slow up Cable’s advance. EUR/USD made new 3-month highs at 1.345 to trade around levels last week in mid-February. USD Index still weak on prospect of stimulus withdrawal weighing on economic fundamentals and continued recovery, but off its worst levels of 80.8.

In Commodities, Gold still in uptrend from June lows, but taking a breather after testing levels of early June. $1350 still serving as support. Upside still possible to $1500 if USD remains weak and Greenback loses safehaven appeal.

Oils still weak on economic uncertainty with US Light Crude down around $104.5 ($3.5 off highs) although Brent is proving more resilient (just $1.4 off highs). Supply concerns and Middle Eastern unrest still helping Brent while WTI suffering from concerns over US weakness from Fed tapering and US Shale boom impact.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Aussie Westpac Leading Index Improved

- Aussie DEWR Skilled Vacancies Improved

- China Conf. Board Leading Econ Index Improved

- Japan Supermarket Sales Deteriorated

See Live Macro calendar for all details