Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

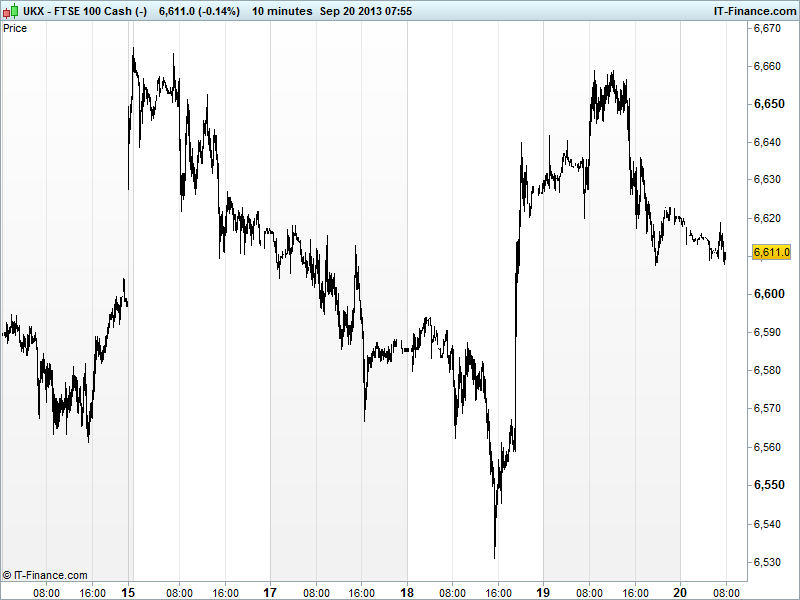

UK 100 called to open -15pts this morning at 6610, with Asian markets flat to lower like their US counterparts amid a subdued end to a big week for expectations and surprises despite a blowout Philly Fed figure. Note many regional bourses closed (CN, SK, HK, TW).

Has the initial reaction to QE for longer run its course already? Would markets have preferred $5bn as confirmation economy doing at least a bit better? Is no taper until, maybe not even until next year, just proof that lots of work still needed? Is the UK 100 back in another sideways channel?

Japan under the cosh despite USD/JPY trading back up above 99, normally a help for exporters, and the BoJ’s Kuroda offering a positive outlook for economies ex-Japan, such as US expecting it to feed through to helping exporters back home and that QE to stay until 2% inflation. Australia in the red (resources) on some profit-taking following yesterday’s Fed generated global rally.

India’s new RBI central bank governor Raghuram delivered his first policy statement and delivered a surprise mix of rate moves. In response to the taper no-show, the World Bank president said delay is positive in short-term while global economy moves into a new phase. Buffet said Fed greatest Hedge Fund in history.

IMF’s Lagarde said growth subdued but advanced economies in better place that 6-months ago and urged US Congress to sort out differences before budget and debt ceiling which is likely to steal the attention from the Fed now. Berlusconi thankfully says will continue to support government as long as policy agreements respected.

In focus today, it’s all still about central bank communication with little data of note bar UK public finances and Eurozone consumer confidence. With Fed members having been so quiet in the run up to the FOMC meeting, updated views after European close are keenly awaited in terms of any additional colour on Bernanke’s statement. German elections this Sunday, with Merkel hoping for a 3rd term.

Estate Agency Foxtons (FOXT) sees conditional trading for its IPO start this morning until Tuesday 4.30pm, with unconditional trading starts on Wednesday. Demand has been high and the pricing already narrowed to the upper end of the proposed range (190-230p). Early indications showing an open above the top end of range.

In FX, USD index off its worst levels of 80.2, but still well off highs of 81.9 at the beginning of the week, thanks to Fed keeping QE3. GBP/USD off its best levels of near 1.62 after USD rebound. EUR/USD holding around 1.355.

Gold holding at $1360 after its Fed-inspired rebound. While the old trendline of raising support serving as become resistance, $1350 could also become support for sideways move.

Oil also off worst levels of overnight at with US Light Crude at $105.5 and Brent at $108.5. Although off best levels of yesterday, both showing some tentative signs of rising lows for support.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- IN Interest Rate Surprise Increase

- JP Nwide Dept Store Sales Improved , Rebound

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- British estate agent Foxtons valued at $1 bln in London listing

- Hochschild’s Inmaculada project on track to start in Q2 2014

- JLT to buy Towers Watson reinsurance brokerage unit for $250 mln