Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

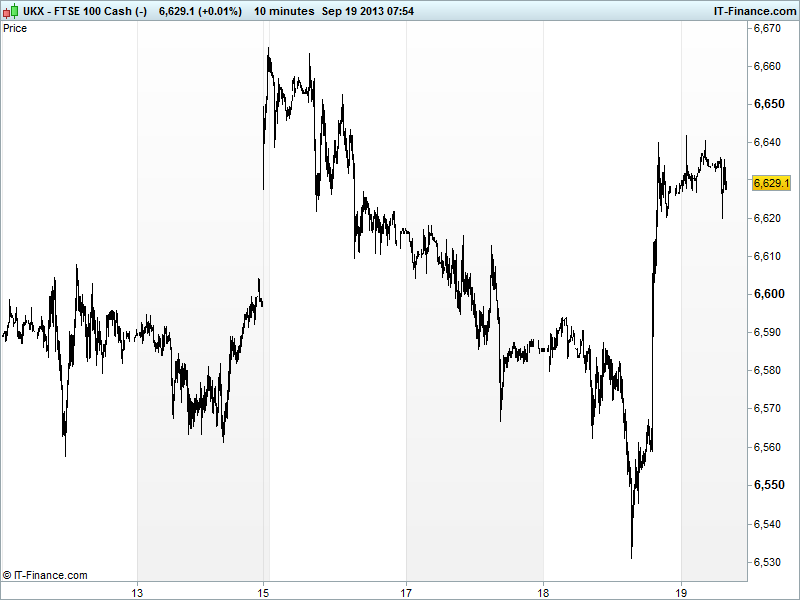

UK 100 called to open +80pts this morning at 6630, back up above the week’s falling highs and longer-term falling trendline since May, thanks to US Federal Reserve surprising markets by not tapering its $85bn QE3 as consensus expected.

Bernanke said data not sufficiently good, political headwinds (budget, debt ceiling) and tighter financial conditions (due to Fed’s June comments about potential tapering). Evidence of sustained improvement needed. Tapering not a given for this year. Très dovish.

As we said yesterday, tapering hopes/fears to bumble on for months on top of Obama political and fiscal struggle with congress. Maybe tapering at year-end after another last minute solution to White House and Congress dispute and some better US data.

Emerging markets reacting positively to the news having suffered from the summer prospect of tapering, and capital flowing back to the developed world as returns became more attractive on a safety basis. Developed markets also reacting well with US equities closing +1%, the S&P& Dow at new record highs and Asian markets higher.

While US bonds rose on the prospect of more bond buying by the Fed, taking yields [and hopefully consumer financing costs] down, the weaker USD also helped both Gold and Oil surge, with the former back up above $1350 and the later $3 to the better (WTI and Brent).

Asian markets higher across the board (although several closed for holidays) taking positive lead from US, despite data from Japan showing a 14th straight trade deficit although it did improve on the month and exports improved at the fastest rates in 3 years thanks to Abe’s stimulus and the weaker JPY. Nikkei gains in-line with region, despite the weaker USD meaning the JPY actually strengthened overnight. New Zealand GDP beat consensus.

In other news, Syria’s leader Assad has said he will fully commit to the chemical weapons agreement. Washington Post quotes White House Official saying Janet Yellen is front-runner for Fed chair adding to last night’s dovish statement by Bernnake. Ratings agency S&P also put Portugal on negative watch on the basis that reforms might fail, although peer agency Fitch says Eurozone reached cyclical turning point and sees stronger US growth.

In focus today will predominantly sit with the fallout from the Fed taper no-show, but we do have UK Retail Sales seen more flat in August but with CBI sales trends improving from flat. US Jobless Claims (even if much improved, Fed still not happy with employment situation) seen returning to real recent level after last week’s IT anomaly. US Existing Housing sales seen weakening a bit in August (likely due to tighter financial conditions the Fed was unhappy about) and Philly Fed ticking up a touch in September.

In FX, USD index down at base of recent tight 81.4-81.8 range. GBP/USD powered higher to 1.61 to close in on 1.63 highs of 2012 (excluding NY spike) and long term falling highs since August 2009. Also helped by BoE minutes. EUR/USD also jumped to above 1.35 now eyeing highs of February near 1.37.

Gold recovered from foray sub-$1300 thanks to Fed announcement – a product of weaker USD making it cheaper and continued QE3 raising prospect of inflation even if it is far from a level that needs hedging or indeed near Fed target. Now testing prior trendline of rising support at $1370. Support now possible at $1350.

Oil jumped on prospect of more easy money helping growth with US Light Crude back up at the $108 levels of mid-month and Brent at $111.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- JP Trade Balance Beat, Improved

- JP Exports Beat, Improved

- JP All Industry Activity Beat, Improved

- JP Leading Indices Improved

- CH Trade Balance Miss, Improved

See Live Macro calendar for all details