Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

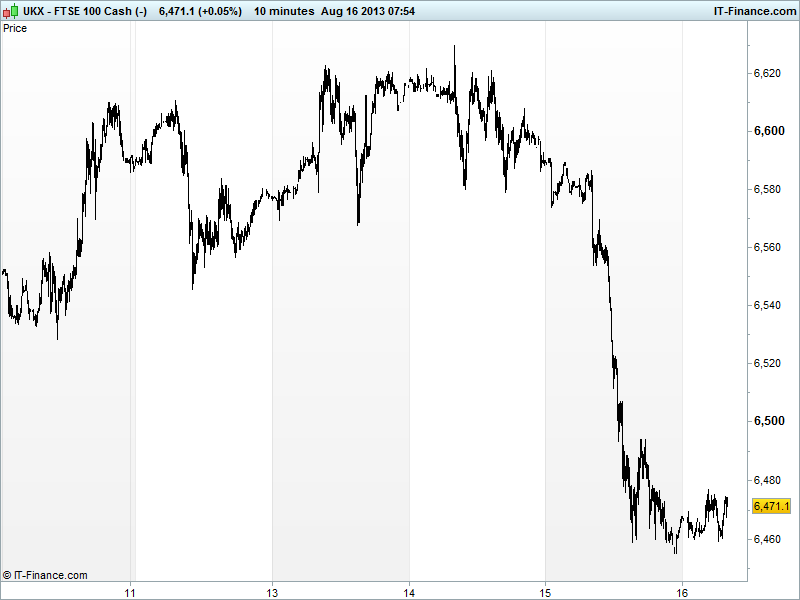

UK 100 called to open -10pts at 6475, after a significant tumble yesterday driven by more intense Fed stimulus tapering fears following US macro data which added to the uncertainty, with jobless claims near pre-crisis lows, inflation ticking up towards target and housing at highs but national production flat and regional manufacturing lower.

Add to this a cut in global guidance by WalMart and Cisco announcing more job cuts and the current situation and outlook are even more muddied, especially when Chinese slowing fears can be countered with a surge in demand for Copper (For exports? Stocking up? Replenishing stocks?) and renewed unrest in the Middle East and the calm of the summer has been stirred up.

Overnight, Asian stocks taken the negative lead from Europe and the US with bourses mostly lower although Shanghai shows solid gains despite some erratic moves linked to speculation (it is Friday) of potential policy support, cuts to the RRR, and futures expiry. Nikkei weak on relative strength of JPY due to weaker USD.

Merkel added to the good tidings by saying the Euro crisis is not over, likely using it as an excuse to say “keep me in power, we’re almost there’, and added she won’t raise taxes. Bullard maintained his stance that more data is needed before the Fed’s FOMC can make its decision son tapering (still managing Fed-spectations) although a think tank report suggests most voting members believe enough data out there to warrant a September move.

In focus today will be the US data again, as investors look for more clues on US growth and the future of the Fed’s QE3 programme. Non-Farm productivity is seen maintaining similar growth to Q1, although unit labour costs are seen rebounding. After the strong housing print of yesterday, starts and permits watched for continued signs of consumer confidence.

July Eurozone inflation seen confirmed as benign keeping the door open for ECB president Draghi to cut rates if necessary to foster the improved data and regional recovery of late. To close the week, the preliminary \official US consumer sentiment figure from the Uni of Michigan is seen just a touch higher consistent with the improving labour and housing data and at multi-year highs, likely adding to the September taper talk.

The UK 100 fell a significant 130pts at one point yesterday and many will be eyeing the overnight support at 6460 and recovery of short-term momentum as boding well for a recovery from the lows of the summer range. The longer term graph still shows a lack of momentum suggesting the possibility of overnight support being merely just a pause before a sequel to yesterday’s clear-out – 6400 and the 200-day MA anyone?

In FX, the strength of belief in a UK rate hike appears to have trumped the prospect of Fed tapering with Sterling winning the GBP/USD war and taking the pair well above the 1.56 level and above the trio of prior resistance (falling highs, 200-day MA and 50% Fibonacci). 1.56 could now revert to support with resistance at June highs 1.575. EUR/USD spiked up to 1.335, but remains in August 1.32-1.34 range. USD Index back down near August lows 81. Still falling highs.

In Commodities, Gold benefiting from weaker USD and now above the $1350 level, which should revert to support. Uptrend from June lows intact, but $50 above trendline. Oil still benefiting from supply concerns and Middle Eastern unrest although Brent is the one trading above prior highs.

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Anite trading in line with expectations

- Atkins sells U.S. construction unit Peter Brown

- RSM Tenon says minimal value seen in Baker Tilly deal

- Bellzone says confident on Kalia project

- Sage says Paul Harrison steps down as CFO

- Severfield Rowen says in line with expectations

- Essar Energy first-quarter Stanlow throughput drops slightly

- Rio Tinto to Cut 1,700 Jobs at Oyu Tolgoi Mine