Markets Overview: (Source: Bloomberg, FT, Reuters, DJ Newswires)

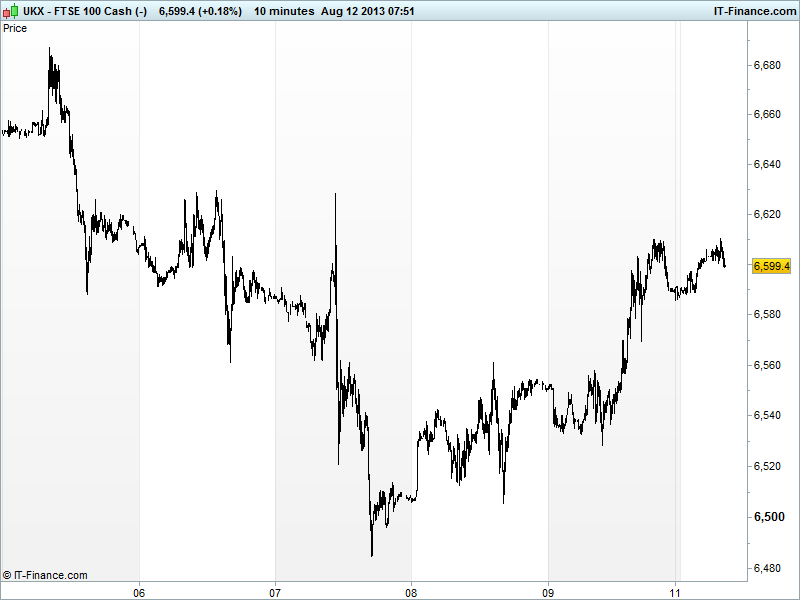

UK 100 called to open +15pts at 6600, maintaining the rebound from late last week on data from China which suggested growth both internationally and domestically as well as inflation prints which imply more room for stimulus to keep growth up above the 7% level which concerns so many on an international scale in terms of the contribution of the world’s #2 economy to the global recovery.

European bourses also called higher in spite of Japanese Q2 GDP figures coming in below expectations and sparking fears that a planned sales tax hike could be damaging to the Abenomics economic revival strategy. Although inflation data did come in hotter that expectations showing the new PM’s strategy is working, although inflation and slower than hoped growth are not the combo he’s after.

Asian bourses positive, bar Japan which is suffering from the overnight macro data as well as the weak USD supporting the JPY hindering exporting equities. The rest of the region is still benefiting from the positive Chinese data of last week and talk that Beijing will relax a ban on real estate companies selling shares. Australia higher on the weaker USD and higher commodity prices benefiting miners.

Weekend news included reports in that a new bailout in in the pipeline for Greece after the German September elections with Der Spiegel citing a Bundesbank report expecting EU governments will approve something by early-2014. An RBS report suggests European banks need to shrink balance sheets by €3.2tn to meet Basel III regulations on capital adequacy. Ratings agency Fitch also raised the debt ceiling caps on 6 Eurozone countries (ES, IT, PL, IRE, SL, LV) although tis will not affect sovereign credit ratings.

In focus today, with an empty macro data agenda, will be the build-up to the raft of European data this week including GDP (out of recession?), Industrial Production, inflation, ZEW surveys as well as the UK, where things looking increasingly positive, updates on house prices (still rising?), unemployment (a Carney/BoE pleasing figure?) and retail Sales (summer boost, general optimism?) and inflation seen slowing yet further. BoE minutes will be surgically dissected. Big numbers out of the US this week will be Business inventories and Retail Sales as well as inflation, Industrial Production, Jobless claims and Housing.

The UK 100 has maintained its recovery from late last week, breaking decisively above the 6560 level and eyeing the resistance around 6630 which reduces the chances of a Bull trap as discussed last week. Watch for 6560 to serve as support for any weakness. Regain of early August high of 6715 still looks feasible, especially of data continues to surprise to the upside. It looks like the >3% correction required to digest the late June/July gains has been delivered.

In FX, GBP/USD slowed up by combination of 2013 trendline of falling highs, 200-day moving average and 50% retrace of the fall since the beginning of the year. Support possible around 1.54 breakout. EUR/USD back from its 1.34 highs but support possible around 1.33 prior resistance. USD/JPY held around 96-97. USD Index off worst levels of 81.

In Commodities, Gold perked up despite USD strength to regain $1333. Possible reversal of downtrend. Support at $1300 but resistance still likely at recent highs just shy of $1350. Oils rebounded strongly their worst levels (1-month lows).

For any help you may require placing trades or in terms of market information, put a call in to our trading floor – all part of the service.

Overnight Macro Data: (Source: Reuters/DJ Newswires)

- Japan GDP Miss

- Japan GDP Deflator Better

- Japan Domestic Corp Goods Prices Better

- Japan Industrial Production Less weak

- Japan Capacity Use Deteriorated

See Live Macro calendar for all details

UK Company Headlines: (Source: Reuters/DJ Newswires)

- Renew acquires Lewis Civil Engineering

- Genel acquires 40% interest in Adigala block

- Mitie says trading in line with expectations

- Private equity firm SVG Capital posts 23% rise in H1 NAV

- RBS – The government’s 81% stake will not be sold off in the next five years says Business Secretary